Is inflation always a monetary phenomenon?

Is inflation always a monetary phenomenon?

Exploring how changes in money could affect the price of chocolate

This piece is following on from a previous piece that went into some theories of money - where I noted that I was splitting an article explaining Sri Lankan inflation into two, and writing a more technical piece on

. However, this explanation of money is taking on a life of its own, and morphing into what is likely to end up as a series of articles exploring money and inflation in Sri Lanka instead of just two. This current article will only expand on some of the basic ideas behind money and inflation for now - though going into a bit more technical points, it will still be quite straightforward in a way. This also means my explanation of money here is going to be overly simplistic, so please do bear with that. Future articles will likely slowly go into more detail and specifics about the Sri Lankan story.Inflation is always a monetary phenomenon. That was Milton Friedman’s declaration and one that has been a powerful part of the global monetary story. The same was referred to once again in Sri Lanka, when the country went through its sharpest inflationary periods in recent history. But how true is this statement and in what contexts does it really matter? The short answer - in many cases, it is very true, but the mechanism of action could be very different (and possibly counterintuitive).

What does the theory of monetary inflation tell us?

I’ll use the same “chocolate” example as in the previous piece for continuity’s sake to explain both how the monetarist view on inflation is both right but also not necessarily relevant in Sri Lanka’s case.

The basic explanation is that ceteris paribus (in simple English, if everything else remains the same - I guess economists felt left out when lawyers used Latin phrases to sound sophisticated), if there is an increase of money, then prices will rise.

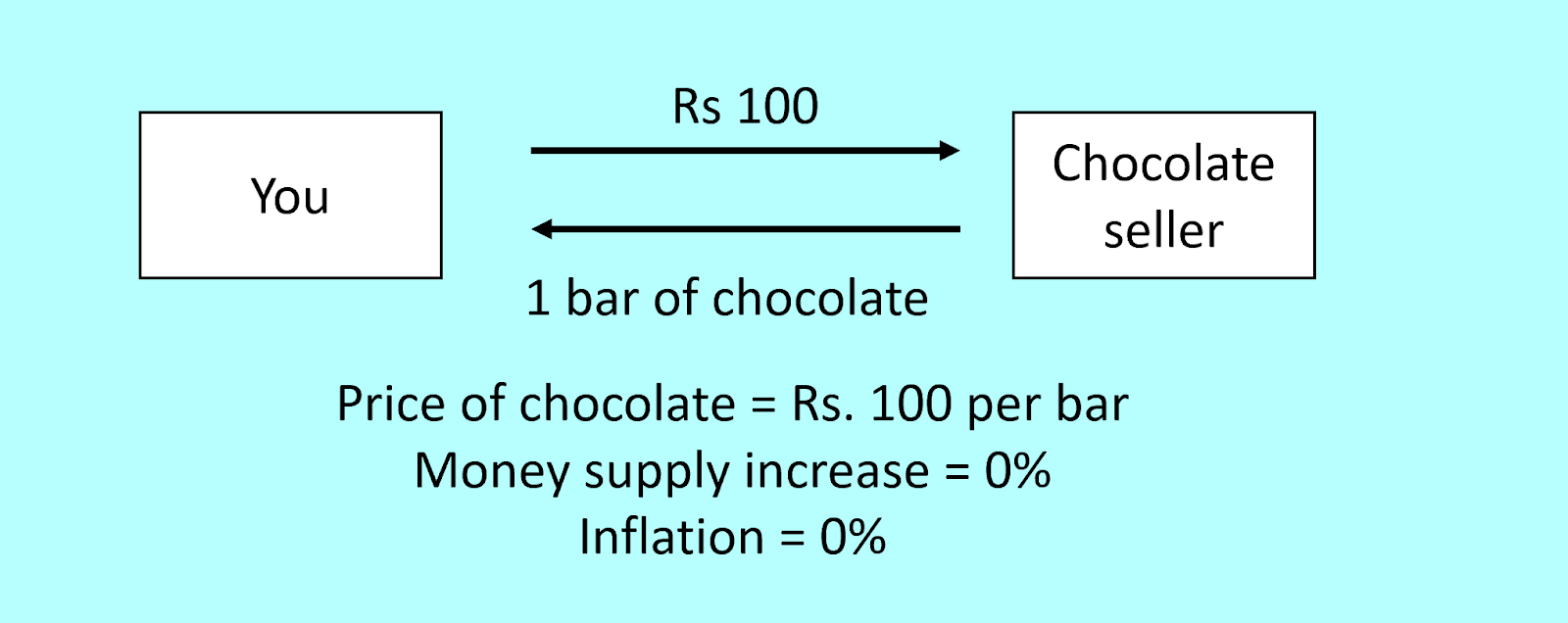

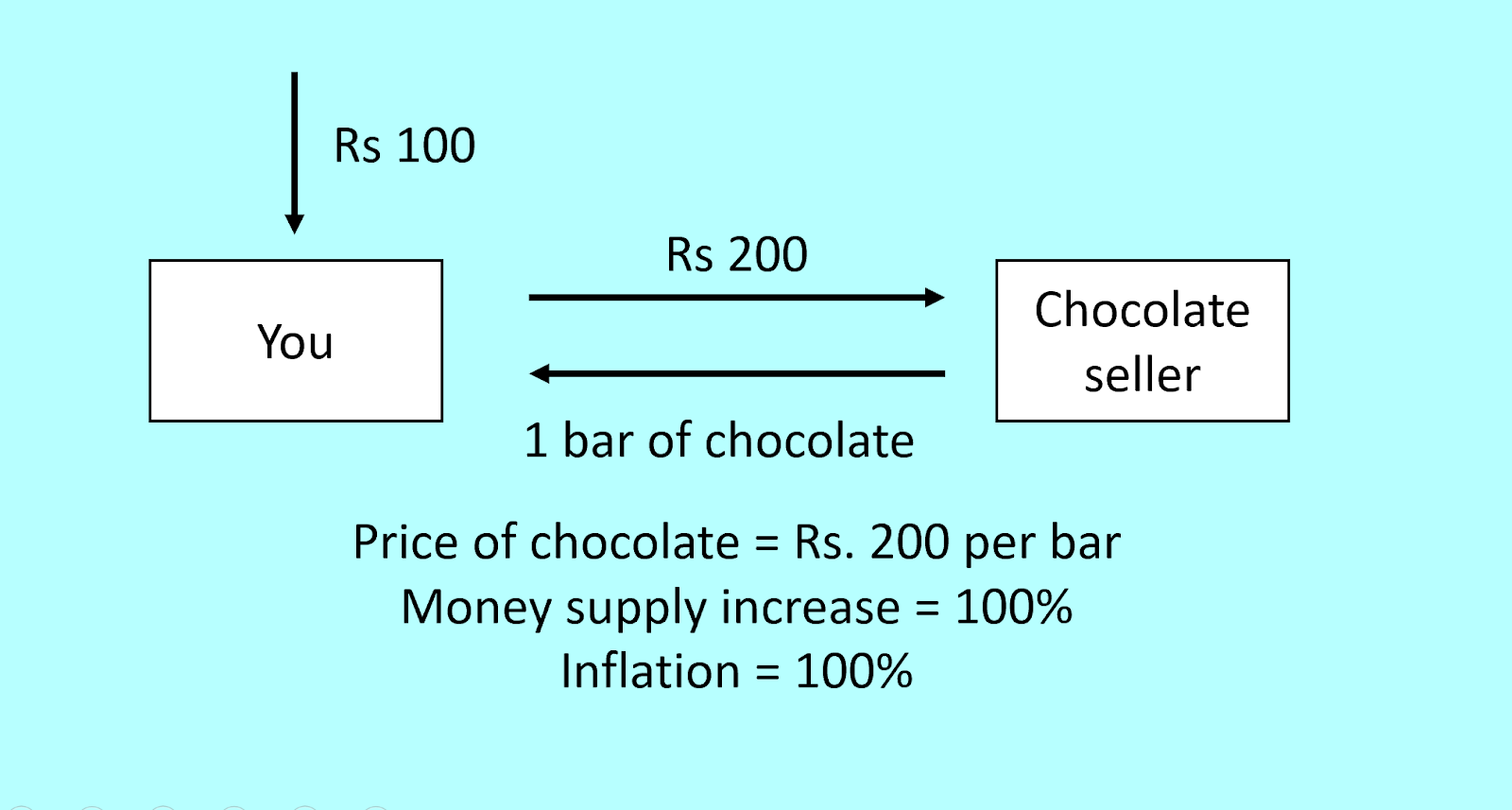

Lets use the chocolate example to assume that you have only Rs. 100, and there is only 1 bar of chocolate, and nothing else in the world. In this context, the price of chocolate is Rs. 100.

If there is a Rs. 100 injection of money, then the price of chocolate will rise to Rs. 200. Money supply has gone up by 100% and inflation is 100% as well.

Reality is more complicated than a simple example - but the relationship still holds broadly

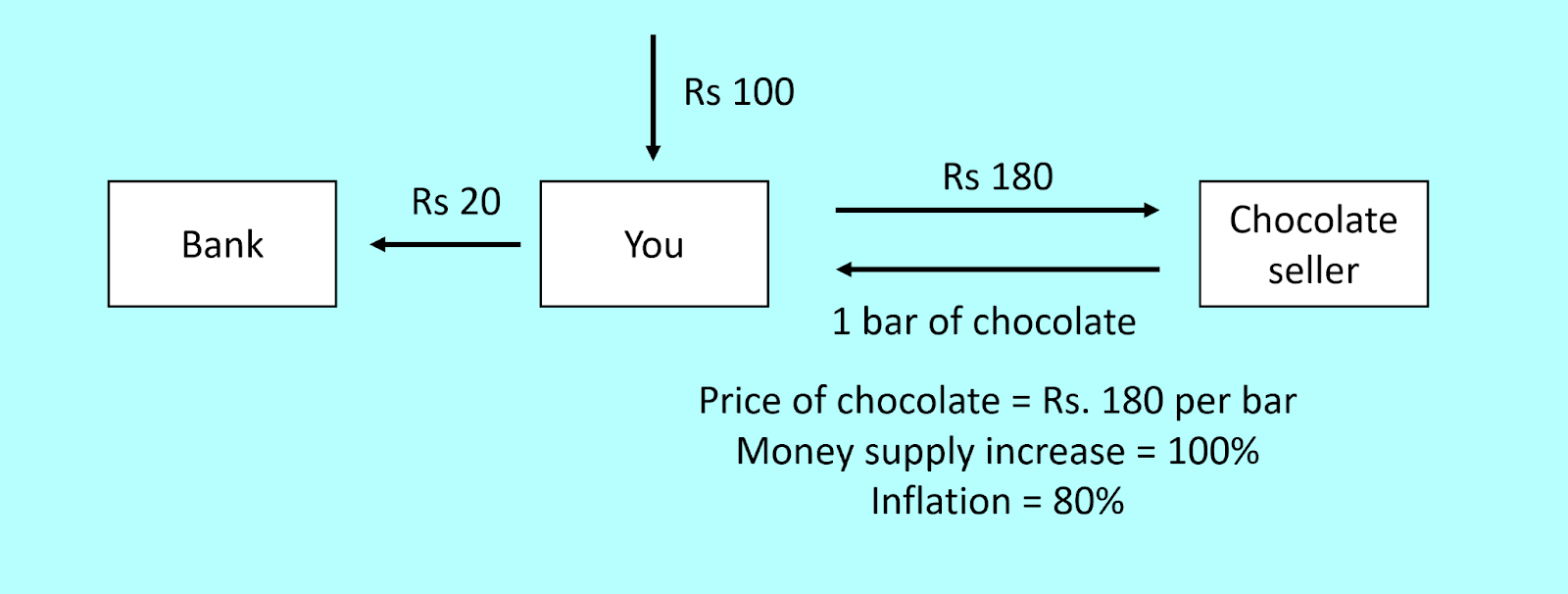

This is the classic monetarist example, but reality is more complicated (you’ll hear me say this many times throughout this piece, please bear with me). Lets assume that you decide to save Rs. 20 of the new Rs. 100 you get, leaving you Rs. 180 to buy chocolate with. Now, though the money supply has increased by 100%, the price of chocolate has only increased by 80%.

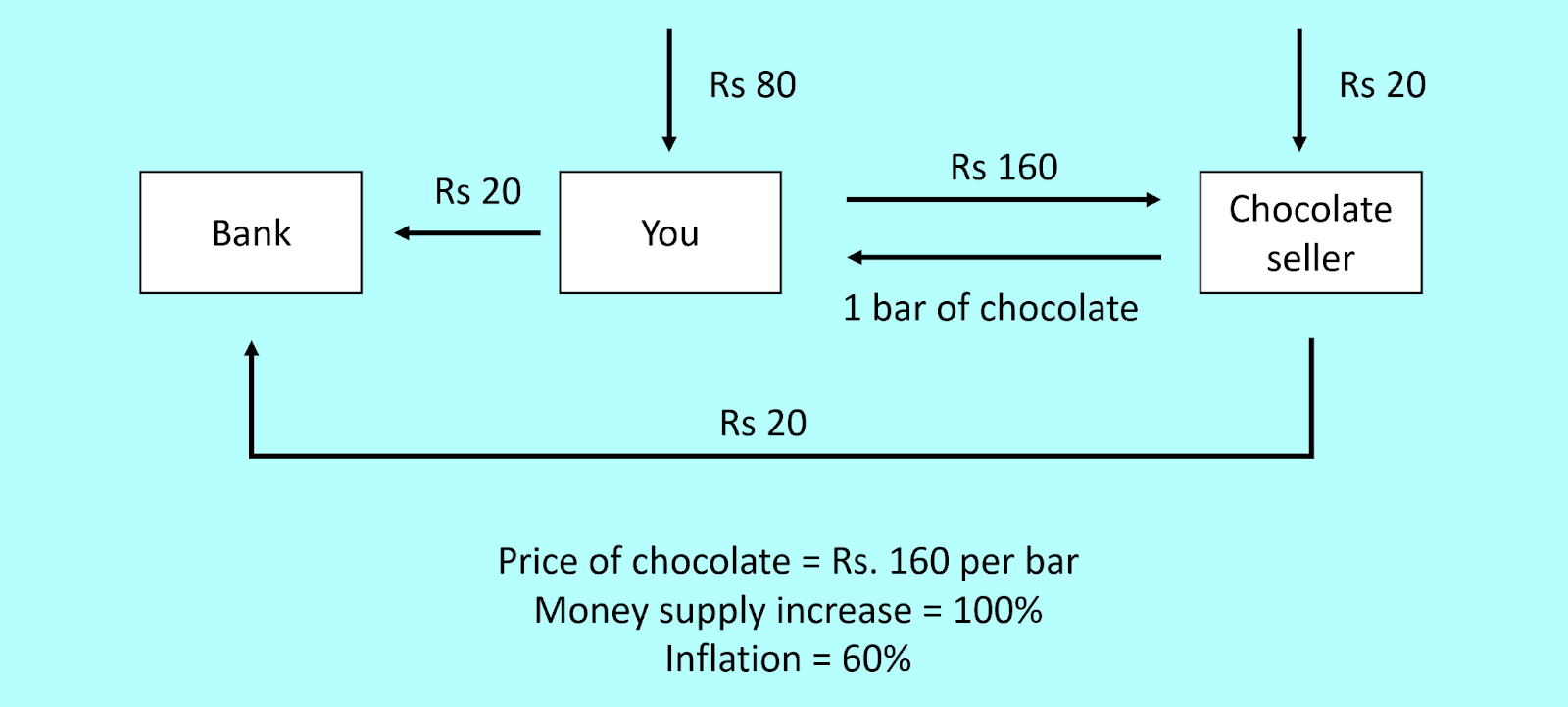

Lets go one step further. Lets assume that the entire increase in the money supply doesn’t come to you alone, but only Rs. 80 comes to you, and Rs. 20 actually goes to the chocolate seller (who saves it). You also save Rs. 20. Now, the total money left to buy chocolate with is Rs. 160, which means money supply goes up by 100% but inflation only rises by 60%.

These examples, although resulting in less than a 1 to 1 relationship, still very strongly suggest that an increase in the money supply definitely does result in an increase in inflation. However, when we started to think about other uses of money outside of goods consumption (for example, how saving in the bank reduces the reality of money available for consumption), we start to see the first inklings of how chocolate prices COULD theoretically, not rise as much as theory suggests.

Money doesn’t always get consumed or saved alone - production can grow too

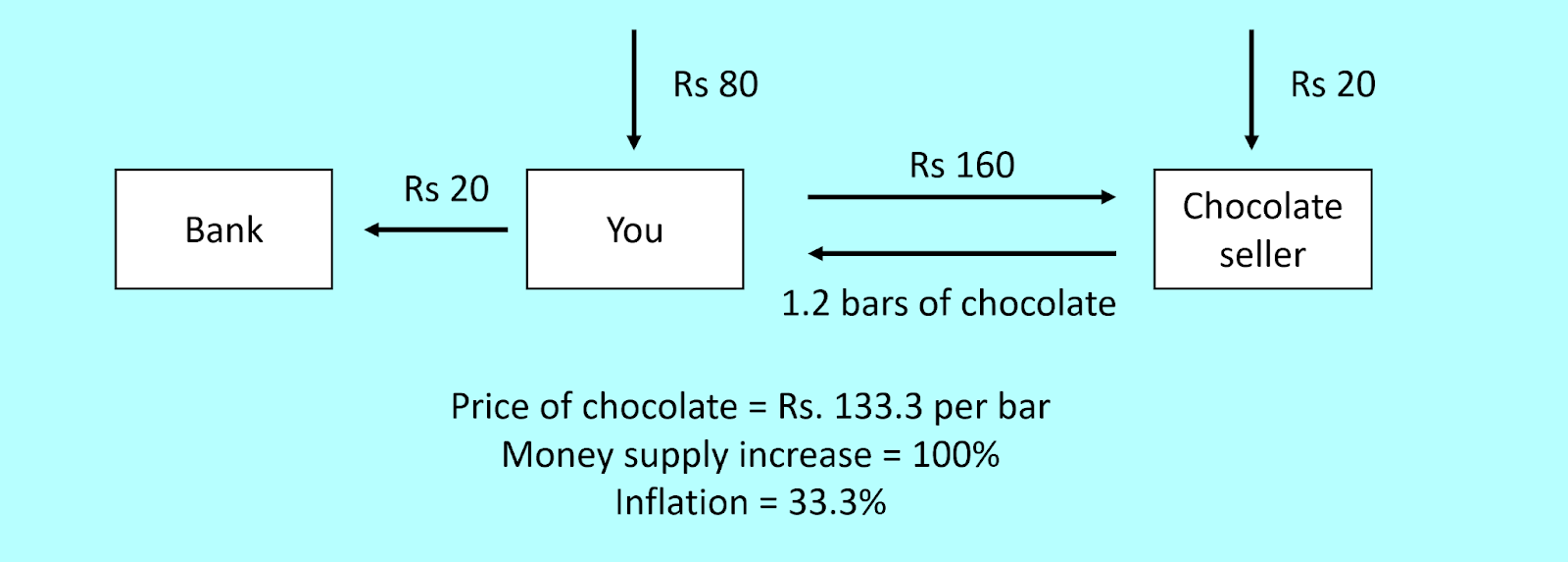

To take this into more contexts, lets take one more step. Lets assume that the Rs. 20 the chocolate seller gets is instead used to increase productive capacity, and now there is actually 1.2 bars of chocolate. The total amount of money left to buy chocolate is still Rs. 160 (original Rs 100 + Rs 80 you got - Rs 20 you saved), but you’re splitting it over 1.2 bars instead. The price of a chocolate bar is now actually Rs 133.3. Although the money supply has increased by 100%, inflation is only 33.3%.

This is of course, a pretty significant difference from where we started off from, although directionally things are still the same. 33% inflation is still high, but I’d argue it means something completely different to the doubling in prices (100% inflation) that the original 1 to 1 relationship suggested. We see this more clearly if we assume this is annual inflation - a 33% annual inflation rate is high, but still in the realm of controllable. 100% annual inflation on the other hand, is bordering on a spill into hyperinflationary territory.

The role of credit in the story of inflation

All our examples so far have involved direct transactions - nothing has been leveraged yet. Lets take another step beyond this to add some credit.

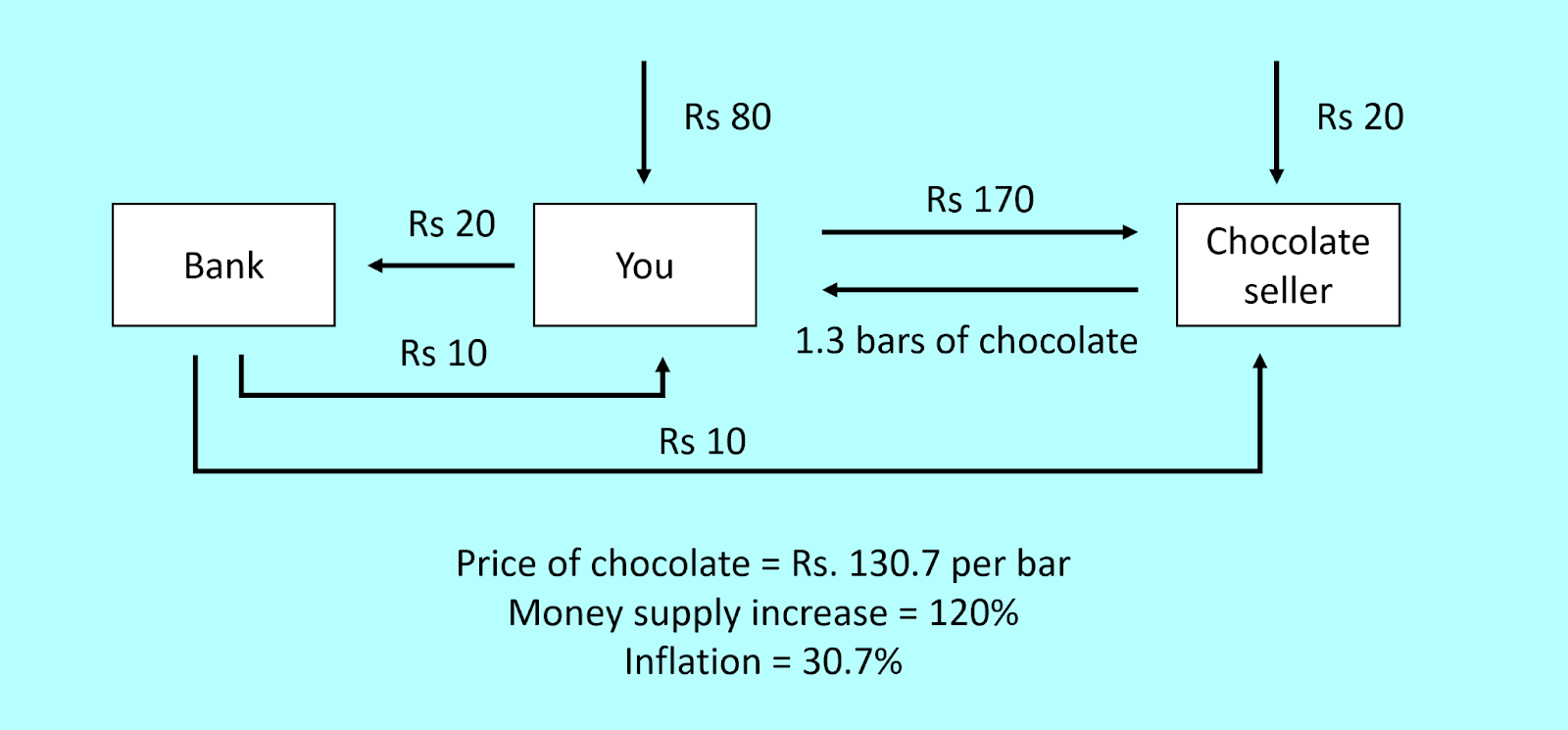

Lets assume that the Rs. 20 you saved is directly lent out by the bank, equally to you and to the chocolate seller (assume no interest). The chocolate seller uses it to expand production even further, to get 1.3 bars of chocolate in the end. For simplicity’s sake, let’s say you decide to use the Rs 10 in credit to buy chocolate as well. Now, the price of chocolate is Rs 130.7 per bar. However, the total money supply has gone up by MORE than 100%, since there is also an extra increase in money due to the credit given by the bank (this expansion in money from credit is a critical point we’ll touch later in this piece, but in more detail another time). Once you factor in the fact that there is an extra Rs 20 due to credit, the relationship between the money supply increase (120% increase) and inflation (30.7%) becomes a little bit less strong again.

This shows a critical point that can be easy to miss when you don’t take this deep-dive. The presence of credit in the economy can THEORETICALLY lead to a situation where inflation FALLS rather than rises, despite an overall increase in the money supply. However, this is contingent on the credit flowing into productive parts of the economy as opposed to the consumption side alone. Lets take 2 examples to show this effect.

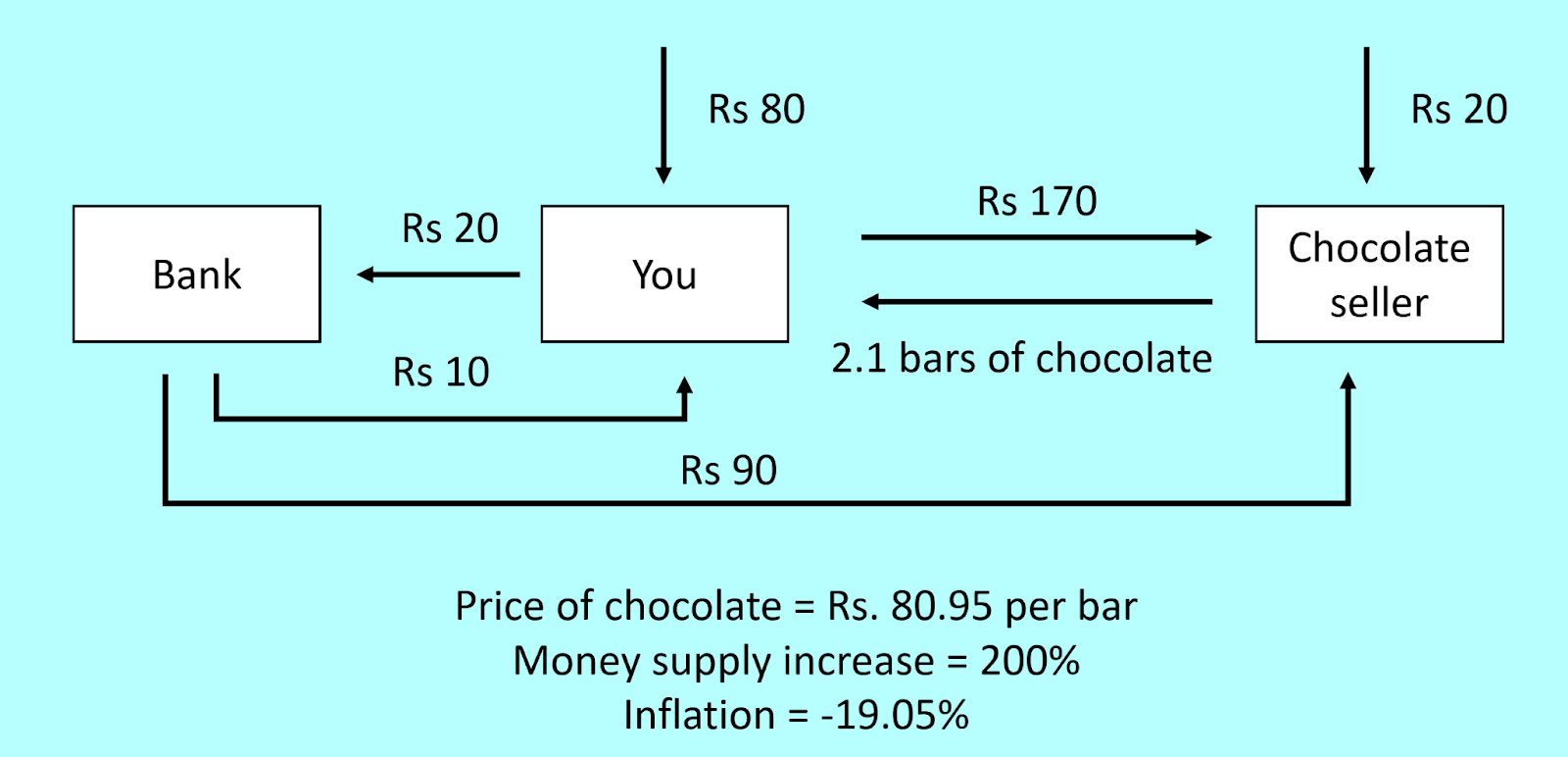

In both these examples, lets assume that instead of only lending out the Rs. 20 that was deposited, the bank decides to lend out a total of Rs 100 (for simplicity’s sake, lets say this is based off money the bank had previously). In these examples, the increase in the money supply is therefore, 200% - Rs. 100 from the initial injection of money, then another Rs 100 in credit from the bank, which adds on to the original Rs 100 you had.

In the first version of this example, the bank decides to lend only Rs. 10 to you (like in the previous example, you use it to buy chocolate again) but Rs 90 goes to the chocolate seller, who uses it to along with the Rs 20 injection to increase production (for simplicity’s sake, lets assume production capacity increases at the same rate as before), and is able to produce 2.1 chocolate bars in total.

Now, for the first time in our examples, we have an actual case of deflation! The money supply has in fact, tripled, but prices have actually fallen instead of rising sharply! Truly a lucky day for the dentist next door. What caused this, however, was that although the money supply increased sharply, a big chunk of the increase went into production, which actually increased the supply of good instead. This isn’t contrary to the monetary theory (which of course, was always ceteris paribus), but it does show how there can be an alternate pathway to how money impacts the system

What about the other example? In the second version of the example we see how the effect of money on inflation is amplified instead. Here, lets see what happens if the bank decides to lend the entirety of the Rs 100 to you to buy chocolate with, lets say because you have land you can show as collateral, and the chocolate seller doesn’t have the same sort of relationship with the bank.

Here, we start to see the powerful impacts of how an increase in money supply can result in sky high inflation. Since the chocolate seller still gets Rs 20 in an injection, production still expands to create 1.2 chocolate bars, but now, you have Rs. 250 to buy it with. Inflation is now higher than 100%. If this stays up, chocolate will soon be unaffordable, and dentists will be out of work too.

The real world is even more complex still - which tilts the balance towards inflation again

All of this could seem to imply that there is a big chance that the inflationary impacts of money can easily be handled, if not prevented altogether. In a highly simple scenario like what we explored (yes, even that was highly simple, even in just the context of the chocolate purchase), that may be true. But again, the real world is far far more complex. Lets explore one final example, the most complex one yet, to show how even in the context of chocolate alone, the real world is far more complicated.

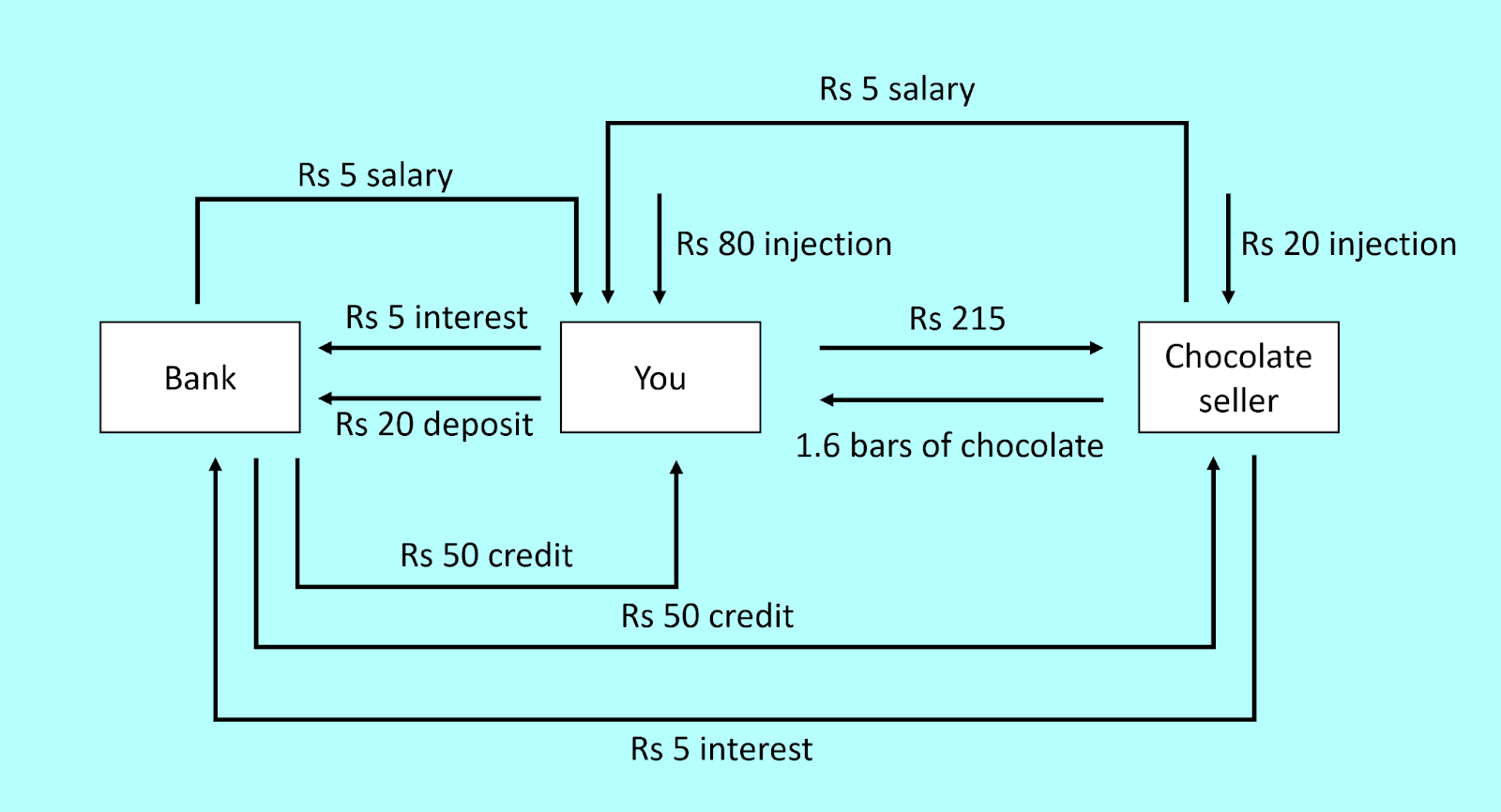

To do this, lets introduce a surprise to the story - you were the chocolate seller all along as well! (i.e. lets assume the chocolate seller is a firm that you have, that you are separately, as a consumer, buying chocolate from). Lets add another twist, and say that you are, in fact, an employee of the bank as well, and thereby, get a salary from the bank too. Finally, instead of the loan being zero interest, lets add a 10% interest rate to the loan, and assume that half of that goes to you as your bank employee salary.

This is a complicated diagram for sure. What’s important is this - due to the second-order effects of the system, consumption rose much more than production. This is because, despite there being an extra Rs 60 going into production (Rs 20 injection+Rs 50 credit-Rs 5 chocolate seller salary-Rs 5 interest), which increased production by 60%, there was an extra Rs. 115 going into consumption (Rs 80 injection+Rs 5 chocolate seller salary+Rs 5 bank employee salary+Rs 50 credit-Rs 20 deposit-Rs 5 interest), which increased consumption much more than the increase in production.

Since the real world is even more complicated than this, this is still just a very basic example for what goes on when money supply increases. But this should still show an important part of the story - when the supply of money rises, prices tend to rise, but this rise CAN be mitigated IF production can also increase. Since investing in productive capacity is a far harder project that just throwing money AND it’s often a longer-term return, the fact that prices can rise in the short-term still rings true.

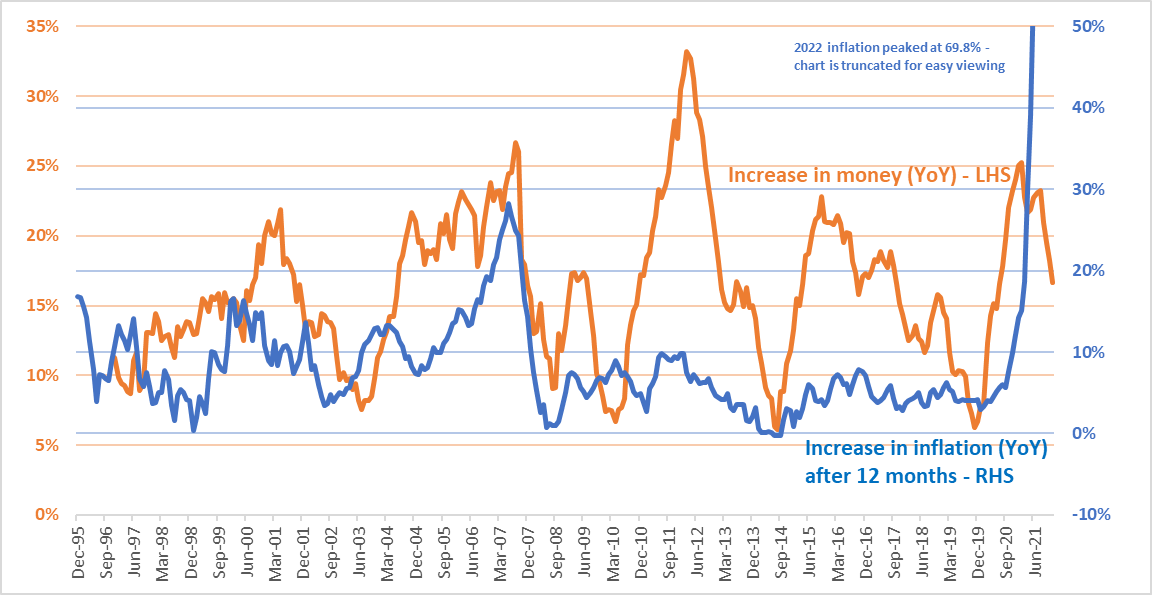

Lets step outside of theory for just a moment, and look at some actual data that shows that the increase in money supply is very much tied to inflation in reality. The following chart shows Sri Lanka’s money supply against inflation twelve months afterwards.

By and large, this chart shows that a rise in money has gone alongside a corresponding inflation increase across the following 12 months. However, the effect isn’t as large as it is implied after 2007 - where inflation didn’t rise beyond 10% despite pretty large expansions in money. This is partly explained by some of the credit factors we discussed, but the far bigger driver that mitigated this, in my opinion, is the movement (or lack thereof) of both the USD and the LKR, which is a story we’ll explore later. Overall, I don’t think it’s unfair to say that Milton Friedman is at least partly vindicated.

Inflation is monetary in the end, but a complicated monetary in many cases

Going through the examples like this also starts to show the absolutely critical role the credit system plays in the inflation story. Governments, which do the direct injections, often have an incentive to give money for consumption (the more people get money, the more votes for the next election - whereas improving production is a more long-term dividend instead). This makes the direct relationship between money supply and inflation much stronger. However, the credit system doesn’t necessarily have that same incentive. What incentives drive the creation of credit in the economy, thereby, can have pretty powerful impacts on inflation, and this is true even when the government itself isn’t directly “printing money” to expand the money supply.

For countries like Sri Lanka, there is an additional channel to all of this - depreciation. Depreciation can causes prices of imported goods to rise (so imported chocolate is more expensive, leading to chocolate inflation again), and the ability of the economy to behave in a way that encourages depreciation also has close ties to credit. This fact is also true when considering that expanding productive capacity doesn’t happen out of the blue, and often involves importing machinery and capacity from abroad, meaning that the deflationary impact of production gain is also reduced in a context like Sri Lanka.

In the end, all of this shows why money, money printing, and inflation aren’t simple stories with simple explanations. There ARE overall narratives that make sense and are broadly correct (inflation being monetary is one of them), but these have many qualifiers, footnotes, and asterisks on top of them. Understanding at least part of the monetary story underneath can therefore help navigate the inflation story for countries like Sri Lanka - and perhaps, make a few more conscious decisions about buying chocolate bars too.

(Thanks to anyone who helped with the story of money so far, particularly